flow through entity taxation

The entitys income only goes through a single layer of tax rather than two corporate tax and shareholder tax. The flow-through entity tax will be imposed on the entitys allocated or apportioned positive business income tax base at the same rate as the individual income tax currently 425.

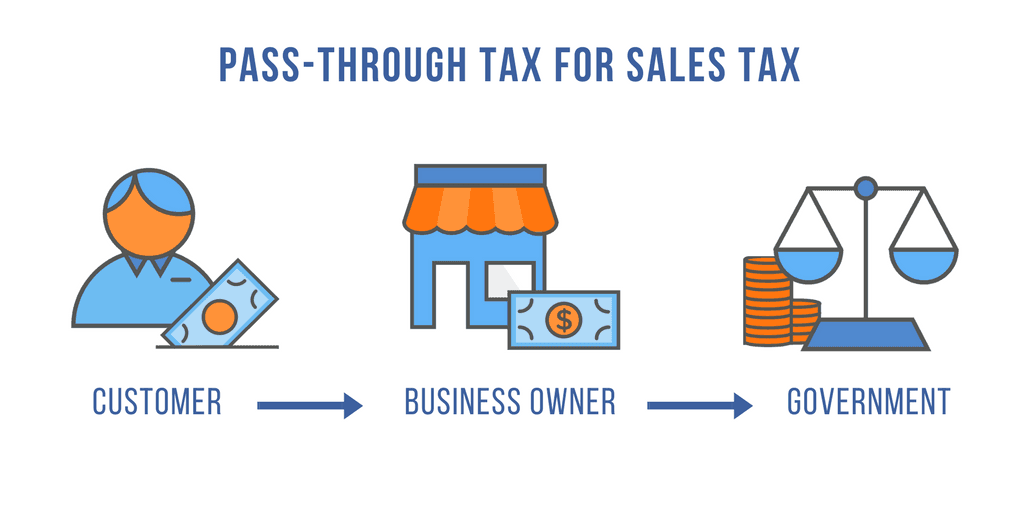

What Is A Pass Through Entity Definition Meaning Example

Flow-through or pass-through entities are not subject to corporate income tax though the Internal Revenue Service does require that they file a K-1 statement annually.

. There are two major reasons why owners choose a flow-through entity. The new tax election option is not available to disregarded entities. The tax is imposed on the positive business income tax base after allocation and apportionment.

The tax base for the flow-through entity tax includes the positive business income of owners who are individuals passthrough entities estates and trusts but not including distributive allocations of loss to a particular owner or the distributive or prorated income allocation to an owner that is a corporation insurance company or financial institution. The flow-through entity tax is computed at the same rate as the individual income tax which for the 2021 tax year is 425. A flow-through entity is a legal business entity that passes income on to the owners andor investors of the businessFlow-through entities are a common device used to limit taxation by avoiding double taxationOnly the investors or.

Flow-through entities are also known as pass-through entities or fiscally-transparent entities. Members of an entity making the election are afforded a refundable credit against their income tax liabilities on their share of the flow-through entitys income. Payments were accepted as early as yesterday but there are specific payment instructions to follow and other considerations before utilizing this workaround.

21 New York Tax Issues for Flow-Through Entities A CCH Seminar Taxation of Resident Individuals A NYC resident pays NYC tax on the same income stream from an S corporation twice at the entity level and on the flow-through income on the individuals personal income tax return. These adjustments which must be performed prior to the. For tax years beginning in 2021 flow-through entities have until April 15 2022 to make this election which will be irrevocable for the next two tax years.

The majority of businesses are pass-through entities. For 2021 the states announcement read that while the initial election into the flow-through entity tax and any payment required are due on certain dates in 2022 many flow-through entities may have wished to make an election or payment on or before Dec 31. Gretchen Whitmer signed House Bill 5376 on December 20 2021 which allows owners of Flow-Through Entities S-Corporations Partnerships the option to pay and deduct their state and local income taxes at the business-entity level instead of individually.

The recently enacted flow-through entity tax allows business owners to deduct Michigan income taxes related to flow-through entities on their federal tax return. Flow-through entities typically pay business income taxes at the individual owner level rather than the entity level and the federal government caps the state and local tax SALT deduction. Once determined the federal taxable income of a flow -through entity is subject to certain specific statutory adjustments.

Common types of FTEs are general partnerships limited partnerships and limited liability partnerships. The associated tax is imposed at a rate of 425 percent equal to the individual tax rate. As enacted this tax is retroactive to tax years beginning on or after January 1.

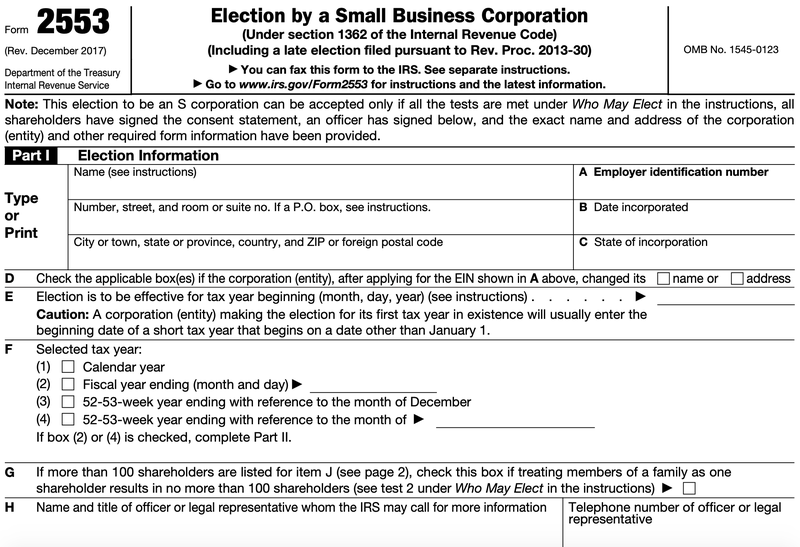

However the website to do so wasnt available until Dec. A flow-through entity FTE is a legal entity where income flows through to investors or owners. The New 20 Pass-Through Tax Deduction.

For tax years beginning on or after January 1 2021 resident partners members or shareholders will be allowed a resident tax credit against their New York State personal income tax for any pass-through entity tax imposed by another state local government or the District of Columbia that is substantially similar to the PTET imposed under Article 24-A. It allows ownersshareholders to receive higher net returns on their investment. Every profit-making business other than a C corporation is a flow-through.

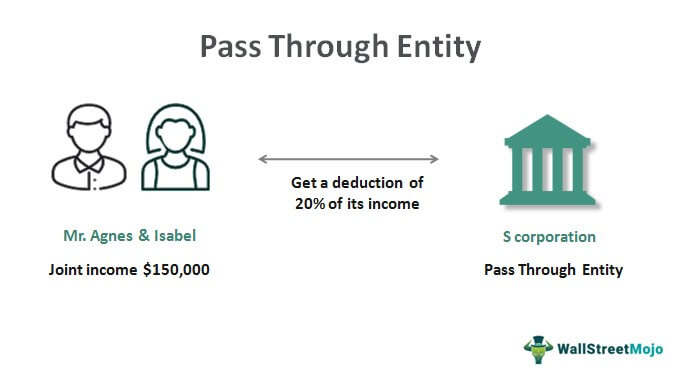

An additional advantage of pass-through entities was created by the Tax Cuts and Jobs Act of 2017 which included a 20 tax deduction for owners of pass-through entities. A pass-through entity also known as a flow-through entity is not a particular business structure but a tax status enjoyed by any business that does not pay corporate tax. For tax years beginning in 2021 the election must be made by April 15 2022.

For tax years beginning in 2021 flow-through entities must make this election by April 15. Generally the flow-through entity tax allows certain flow-through entities to elect to file a return and pay tax on income in Michigan and allows members or owners of that entity to claim a refundable tax credit equal to the tax previously paid on that income. In calculating the tax at the entity level the tax is only computed on the business income tax base allocated to those members who are individuals flow-through entities estate or trusts and exclude the business income tax base allocable to those members that are corporations insurance companies or financial institutions.

This means that owners can deduct up to 20 of the companys qualified business income QBI on their personal tax return. The most typical function of a flow-through entity is to ensure that its owners and investors are not subject to double taxation which is the case for C-corporations. Advantages of a Flow-Through Entity.

For taxable years beginning on or after January 1 2021 and before January 1 2026 qualifying pass-through entities PTEs may annually elect to pay an entity level state tax on income. The Entity Level tax rate is. Qualified taxpayers receive a credit for their share of the entity level tax reducing their California personal income tax.

Common Types of Pass-Through Entities. That is the income of the entity is treated as the income of the investors or owners. This legislation would allow flow-through entities such as S corporations and partnerships to pay an entity-level tax equivalent to the income tax rate.

The flow -through entity tax generally begins with amount s determined and reported by the entity for federal income tax purposes.

A Beginner S Guide To Pass Through Entities The Blueprint

What Are The Tax Implications For An Llc Effects Of Operating As An Llc

![]()

State Pass Through Entity Tax Tracker Baker Tilly

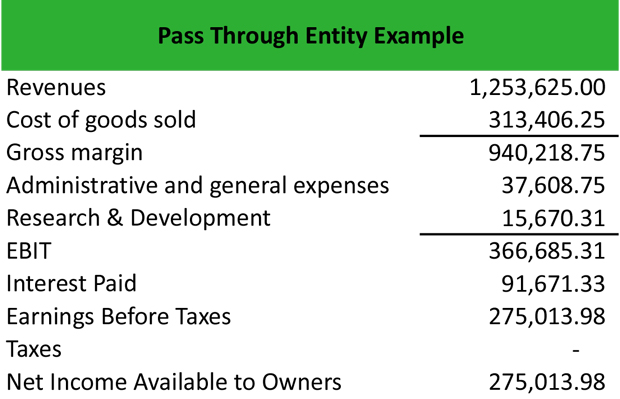

Pass Through Entity Definition Examples Advantages Disadvantages

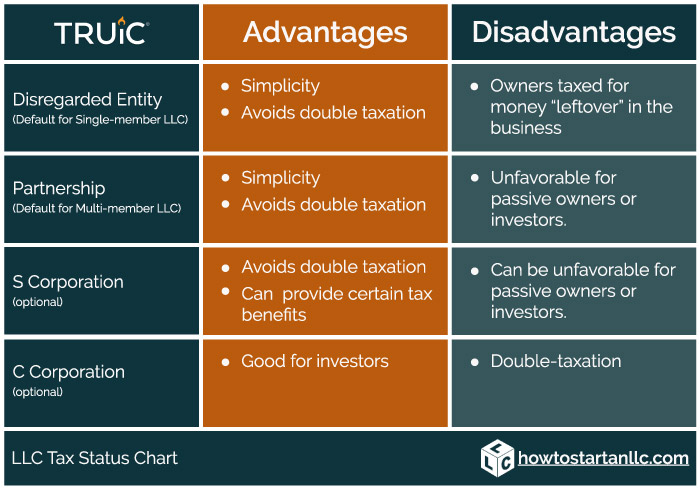

How To Choose Your Llc Tax Status

Jp Magson Private Client Wealth Management

Pass Through Taxation What Small Business Owners Need To Know

Pass Through Entity Definition Examples Advantages Disadvantages

![]()

State Pass Through Entity Tax Tracker Baker Tilly